A quantitative trader I know in Chicago recently sent me a link to an article on TrustedQuant about mean reversion in quant trading. It’s a well-written piece, and the author makes sharp observations about why strategies that look brilliant in backtests tend to fall apart in live markets. Worth a read if you’re curious about how the quant world thinks.

But here’s the thing: almost none of it applies to what I teach.

That’s not a knock on the article. It’s actually the point. Calling quant trading and retail trading “apples and oranges” doesn’t go far enough. They’re not even the same fruit.

What Quant Bros Are Trying To Do (Beyond Showing Off)

The article digs into problems like crowding, execution slippage, correlation breakdown, and hedge ratio drift. These are real problems, and they matter enormously when you’re running hundreds of millions of dollars in a stat arb strategy. At that scale, your position size moves markets. You have to worry about whether you can get filled without alerting the other side. You have to worry about whether your edge has been arbitraged away because fifty other funds noticed the same signal.

A quant desk worrying about whether a 40 basis point expected return degrades to 15 basis points in live trading is dealing with a fundamentally different constraint set. They need all that machinery: cointegration tests, Kalman filters, half-life estimation, rolling z-scores. Their survival depends on it.

What Us Regular Folk Actually Doing

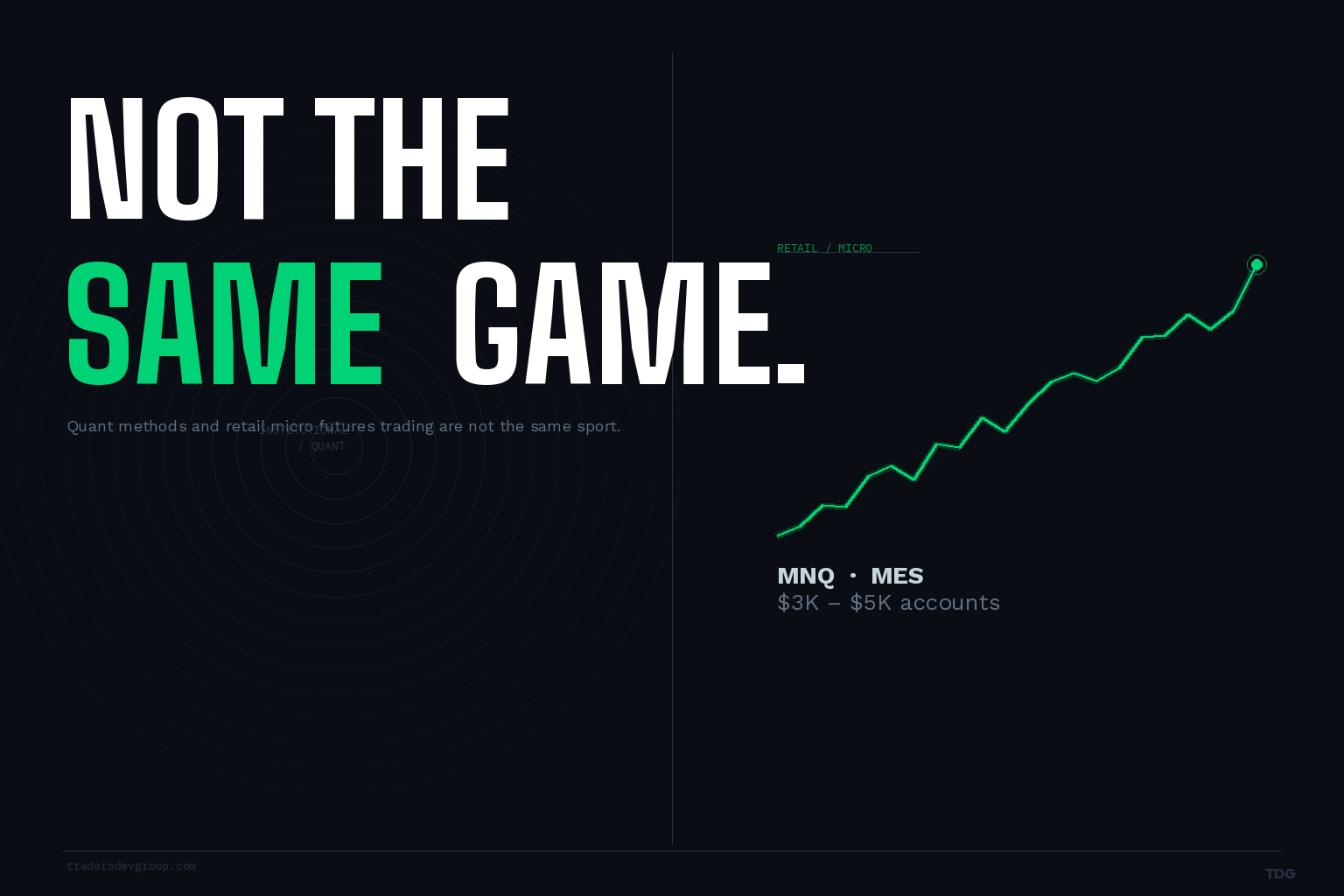

I teach retail traders how to trade micro futures. We’re talking MNQ and MES, instruments specifically designed for accounts in the $3,000 to $5,000 range. The position sizes we’re working with are invisible to the market. We are not moving anything.

That changes everything.

We’re not trying to extract alpha at scale. We’re not managing redemption risk or Sharpe ratio targets for institutional investors. We’re looking for short-term order flow imbalances, clear market structure, and well-defined setups with manageable risk.

The edge isn’t statistical in the quant sense. It’s perceptual and executional. You learn to read what the market is doing, you wait for your setup, and you manage your size appropriately for your account.

The irony is that many quant strategies would love to have our flexibility. A fund running $500 million cannot just flip in and out of MNQ on a five-minute chart. The constraints that make all that quant machinery necessary are the exact same constraints that make the retail approach impossible for them. We have an advantage they don’t: our size doesn’t matter. But, of course, our sizing does.

When Quant Bros Come Knocking

Sometimes well-intentioned quant traders will challenge retail approaches to trend following, mean reversion, breakout trading, or other common strategies. They’ll cite backtest decay, crowding effects, or statistical concerns about the persistence of edge. They’re not wrong about any of that, within their context.

But they’re applying the wrong framework. Those critiques matter when you’re running institutional capital and your returns have to survive transaction costs at scale, plus redemptions, plus regulatory scrutiny, plus competition from dozens of other funds running similar models. For a trader working a $5,000 account on micros, those concerns are simply not the binding constraint.

The binding constraints for our traders are discipline, risk management, proper sizing, and the ability to execute a plan without letting emotions take over. You know, sucking less. No amount of quant sophistication addresses those problems, because they’re not mathematical problems. They’re behavioral ones.

So Here’s The Message

I appreciate the quant world for what it is. It’s intellectually rigorous and there are genuine insights in understanding how markets work at a structural level. But we shouldn’t let someone else’s constraints become ours.

You’re not managing a fund. You’re learning to trade micros in a way that builds consistency and protects your capital. That’s a completely different game, and it deserves to be evaluated on its own terms.

Want to see, hear, and experience how us little guys can pull off alpha generation the smart money could only dream of? Come join the conversation in our trading community — drop your questions, share your charts, and learn alongside traders who are working through the same things you are.

[Join the Discord Community →]

I’m the Chief Button Pusher and founder of TradersDevGroup, a live futures trading education community. Nothing in this post constitutes financial advice. Futures trading involves substantial risk of loss. Past performance is not indicative of future results.

Commodity Futures Trading Commission. Futures and Options trading has large potential rewards, but also large potential risk. You must be aware of the risks and be willing to accept them in order to invest in the futures and options markets. Don’t trade with money you can’t afford to lose. This is neither a solicitation nor an offer to Buy/Sell futures or options. No representation is being made that any account will or is likely to achieve profits or losses similar to those discussed on this web site. The past performance of any trading system or methodology is not necessarily indicative of future results.

CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.